Learned a lot lending an editorial hand here:

PwC Strategy&/Project1932, June 2025

by Fadi Adra, Dr. Shihab Elborai, Chadi N. Moujaes, and Jana Yamani

As the large-scale transformation initiatives in the Gulf Cooperation Council (GCC) countries come to fruition, they require newly skilled and expanded workforces and many new leaders. We estimate that economic diversification, advanced technologies, and the shift to knowledge-based work will create the need for an additional 700,000 top and middle managers in the region by 2030, which is 30 percent more than were required in 2024.

GCC governments have prioritized human capital development, principally through education reforms and workforce localization. These efforts have increased workforce participation of GCC nationals and women significantly. However, they are insufficient to equip young professionals with all the practical capabilities and soft skills necessary to meet the coming workforce requirements.

Mentorship programs, which draw upon the Arab world’s historical legacy of apprenticeship, can bridge that gap. When systematically structured and executed, mentoring fosters the functional and industry knowledge of emerging leaders, hones their acumen and soft skills, and prepares them for the technological advances shaping the future of work.

Findings drawn from Project1932, a Saudi-based initiative cultivating emerging leaders by connecting them with experienced mentors, indicate that the design of successful mentorship programs entails five elements and three enablers. The elements are shared purpose, synergistic matchmaking, a structured and relevant curriculum, mentoring for mentors, and community power. Successful programs are enabled by strong leadership, robust monitoring and evaluation systems, and coherent financial sustainability strategy.

Further, surveys and interviews of Project1932 participants have revealed five insights for fostering mentoring success. Successful programs challenge mentees to leave their comfort zones, train mentors in active listening so they can provide tailored guidance, build strong mentor–mentee relationships, encourage calculated risk taking, and empower mentees to question the status quo.

Project1932 demonstrates that systematic mentorship programs conducted at scale can bridge the GCC’s gap between leadership demand and supply. Read the rest here.

Friday, June 13, 2025

Leadership by design: Lessons in mentorship success from Project1932 in Saudi Arabia

Wednesday, January 15, 2025

Don’t Confuse Ambition With Effective Leadership

Insights by Stanford Business, January 15, 2025

by Theodore Kinni

There’s an old saw — cribbed from Plato and popularized by Douglas Adams — that those people who are most interested in leading others are least suited to the task. That’s not entirely accurate, yet new research has found a grain of truth in this idea: Many leaders have plenty of ambition to lead, but that’s no guarantee others think they’re effective.

“Our society assumes that there is a link between leadership ambition and leadership aptitude,” explains Francis Flynn, a professor of organizational behavior at Stanford Graduate School of Business. People seeking power and success step up to take leadership roles, and how we select leaders rewards that ambitiousness. “We largely rely on opt-in mechanisms to populate our pools of potential leaders — the people who apply to business schools like Stanford or seek a promotion to the next level in their organizations,” Flynn says. “That assumes implicitly that those people who want to lead are the ones who should lead. But is that assumption valid?”

Though it is clear that ambition plays a significant role in who becomes a leader, its link to leadership effectiveness has not been extensively studied. So Flynn, with Shilaan Alzahawi and Emily S. Reit, PhD ’22, undertook the first systematic study of that relationship. Read the rest here.

Monday, December 9, 2024

ASX 100 CFOs Unlocked: Identifying the Leadership Advantage that counts

Learned a lot lending an editorial hand here:

Spencer Stuart, December 2024

by Jean E. Chiswick and Lucy Smith-Stevens

A senior leadership position, one pivotal to company performance, has undergone a profound shift.

Today’s chief financial officer (CFO) must influence beyond financial issues and offer cross-enterprise leadership on a range of different challenges. The role requires strong communication — someone able to seamlessly switch from internal to external audiences on a range of contemporary industry themes. They have to deftly navigate opportunities and risks, juggle a myriad of stakeholders and be co-pilot to the chief executive, working shoulder to shoulder in many cases, both inside and outside of the company.

No wonder the CFO so often looms large as a strong candidate when a CEO succession is underway.

But it’s not always smooth sailing.

The last two years have been pockmarked by a variety of economic challenges, increased complexity and ambiguity, as well as intense geopolitical disruption. Perhaps unsurprisingly, we have observed a shift in ASX 100 CFOs appointed with more proven CFO track records, classical accounting backgrounds and established credibility in public markets.

Does this mark a return to linear pathways to ASX 100 CFO succession? Well, not necessarily. We have found that 25% of internal CFO promotions have had exposure to P&L or operational leadership positions. This shows that breadth of experience is still important.

With more proven CFOs appointed in ASX 100 CFO positions, coupled with growing CEO succession from CFO roles, one thing is clear: an experienced CFO is the leadership advantage that counts. (Read the rest here.)

Wednesday, May 8, 2024

‘I’m Sorry, Dave.’ When AI Writes a CEO’s Apology Letter.

This Week in Leadership, May 8, 2024

by Theodore Kinni

Generative artificial-intelligence programs are already helping professionals write compelling sales presentations, convincing emails, and other difficult business communications. It was only a matter of time before someone tried using it for one of the most sensitive documents of all: an apology from the boss.

Using the widely available GPT-4, researchers at the Korea Advanced Institute of Science and Technology (KAIST) recently built a model they call “Prompt Engineering for CEO Apology.” The model incorporates a number of variables, including type of event, structure and length of previous apologies, audience, delivery method, and the communication styles of the CEO and the company. The researchers used the model to create apologies for some recent high-profile CEO gaffes, and apparently, AI did pretty well: According to the KAIST study, the notes “conveyed empathy” and “mimicked the same structure and emotional language” of CEO apologies produced by human beings. Read the rest here.

Monday, March 25, 2024

Skills-Based Hiring: Where Did It Go?

This Week in Leadership, March 25, 2024

by Theodore Kinni

But only one word describes how often non-degreed applicants appear to be getting hired: rarely. A new study from the Burning Glass Institute and Harvard Business School’s Managing the Future of Work program uses employment ads to track the progress of skills-based hiring. It found that from 2014 to 2023 the number of roles for which employers dropped degree requirements increased fourfold. But when they studied a sample of 11,300 of these roles, they found that the share of workers hired without a college degree grew by only about 3.5% in 2023. Extrapolating its findings across the hiring universe, the team concludes that “for all its fanfare, the increased opportunity promised by Skills-Based Hiring has borne out in not even 1 in 700 hires last year.” Read the rest here.

Monday, November 13, 2023

How to Productively Disagree on Tough Topics

Learned a lot lending an editorial hand here:

MIT Sloan Management Review, November 13, 2023

by Kenji Yoshino and David Glasgow

Neil Webb/theispot.com

Conversations about identity, diversity, and justice are some of the thorniest human interactions of our time. Consider Uber’s head of diversity, who hosted a workplace event titled “Don’t Call Me Karen” to highlight the “spectrum of the American White woman’s experience” and foster an “open and honest conversation about race.” Following backlash from employees of color, she was placed on a leave of absence.

Tuesday, June 13, 2023

Risk Intelligence and the Resilient Company

Learned a lot lending an editorial hand here:

MIT Sloan Management Review, June 13, 2023

by Ananya Sheth and Joseph V. Sinfield

Simon Prades

Business resilience is a dynamic property that is retrospectively measured by the stability and longevity of corporate value across changing contexts. In real time, it manifests in an enterprise’s timely adaptation to both immediate and gradual changes in the business environment.

Our work, which employs a complex adaptive systems view of businesses, shows that resilience derives from three fundamental adaptive capacities: sensing and monitoring, to recognize emerging changes in the business environment; business model portfolio development, to build and test capabilities across operating contexts; and fundamental capability development, to drive growth with longevity and avoid corporate stall. Moreover, each of these capacities hinges on the development of a capability for risk intelligence.

We define risk intelligence as the honed ability to rigorously interpret risks and the consequences or opportunities they pose for a company. It allows leaders to see through environmental complexity and systematically identify, categorize, and interpret risks. This enables them to look beyond known risk factors and intentionally explore yet-to-be-known risks, thereby embracing rather than avoiding uncertainty. Importantly, risk intelligence brings recognition that individual risks or the forms in which they manifest matter far less than the often-shared consequences they have on a company’s value exchange system — that is, the manner in which it manages, identifies, creates, conveys, delivers, captures, protects, and sustains value. And finally, it provides leaders with a network view of risks that enables more effective allocation of risk mitigation resources by illuminating not just the direct consequences of risks but the manner in which they could cascade across the company’s value exchange system. In this article, we break down risk intelligence into actionable elements that leaders can pursue to help toughen their organizations for the long term. Read the rest here.

Monday, June 5, 2023

How to move the needle on innovation

strategy+business, June 5, 2023

by Theodore Kinni

Illustration by Luis Alvarez

As CEOs continue to call employees back to the office, their rationales often include remote work’s deleterious effects on innovation. There is some basis for these claims: a recent study found that the number of email exchanges between research units at MIT dropped by 38% during the pandemic lockdown. Its authors equated email volume with the weak ties that are crucial to the diffusion of information and ideas in networks, and thus concluded from the drop in traffic that remote work hinders innovation. But no matter how much weight you assign this finding, it’s a stretch to peg the success—or failure—of a company’s innovation efforts to the number of rears in seats.

The truth is innovation in large companies is a perennial challenge for leaders, no matter where employees are working. The late Clayton Christensen and other researchers detailed the obstacles to innovation that arise when industry-leading companies confront disruptive technologies. Large companies also struggle to transform innovation investments into financial results: in 2018, consultants from Strategy&, PwC’s global consulting business, examined 15 years of data drawn from the firm’s Global Innovation 1000 research—an annual analysis of the 1,000 publicly held companies that spend the most on R&D—and concluded, “There is no long-term correlation between the amount of money a company spends on its innovation efforts and its overall financial performance.”

So how can leaders move the innovation needle in big companies? I turned to Lorraine Marchand for answers. Marchand served in a variety of executive and board positions, including a former stint as general manager of the life sciences division of IBM’s Watson Health (now Merative), before writing The Innovation Mindset: Eight Essential Steps to Transform Any Industry — a practical guide to building innovation prowess across an organization — and founding her own innovation consultancy.

Here is her list of ways to make your company more innovative. Read the rest here.

Wednesday, March 15, 2023

When It Comes to Half-Truths, No News Is Bad News

Insights by Stanford Business, March 15, 2023

by Theodore Kinni

iStock/PeopleImages

Voluntary disclosures, like those issued by managers in quarterly earnings calls, inform investment decisions across financial markets. They can buoy — or puncture — corporate valuations and stock prices. But it isn’t always clear what effects result from the policies governing these disclosures, especially when it comes to rules about half-truths and the duty to update.

In a new article in Management Science, Anne Beyer, a professor of accounting at Stanford Graduate School of Business, and Ronald Dye of Northwestern’s Kellogg School of Management, use static and dynamic models to understand the effects of regulation on both voluntary corporate disclosure policies and the investors who depend on them.

Half-truths are disclosures that are true in and of themselves but misleading in light of other information managers know but choose to withhold. For example, if a company announces that it will be losing one of its major customers but doesn’t mention that it’s also aware that another major customer is likely to leave, that would be a half-truth. These kinds of omissions are illegal under federal securities law, but their definition is not universally agreed upon. This creates loopholes that can make it difficult to hold managers legally accountable for skirting the whole truth.

Legality aside, whether permitting half-truths in disclosures is preferable to prohibiting them is an open question. Many disclosure regulations aim at providing transparency for investors and other stakeholders. However, it is not self-evident whether barring managers from issuing half-truths leads them to disclose more information.

On the one hand, if a prohibition of half-truths is enforced, then a firm that wants to make a disclosure must disclose the entire truth and cannot selectively withhold part of the relevant information. This may cause the firm to not make any disclosure. On the other hand, if half-truths are allowed, a firm may be willing to share some information on a topic that it would be unwilling to share if full disclosure was required. Read the rest here.

Tuesday, March 14, 2023

Profiles in burnout

strategy+business, March 14, 2023

by Theodore Kinni

Photograph by PeopleImages

It would have been more surprising if the PM had, as she described it, “a full tank, plus a bit in reserve for those unplanned and unexpected challenges that inevitably come along.” After all, she led New Zealand through a series of major crises, including the covid-19 pandemic and the Christchurch mosque shootings, which were the worst terrorist attacks in the country’s history. She endured extreme abuse online and received an unprecedented number of personal threats—so many that she may be the first ex-PM in New Zealand to require high levels of security. And she became a parent while PM, giving birth to a daughter, now four years old.

Going by The Burnout Challenge, by Christina Maslach and Michael Leiter, Ardern’s five-year-plus run as PM was a perfect storm for burnout. The authors should know. Maslach, who is professor of psychology emerita at University of California–Berkeley, created the Maslach Burnout Inventory, the first and leading burnout assessment, in 1981. Leiter, who was a professor of organizational psychology at Australia’s Deakin University and held the Canada Research Chair in Occupational Health at Acadia University, has been researching burnout—and collaborating with Maslach—for almost as long. Read the rest here.

Friday, March 3, 2023

Beware the Pitfalls of Agility

Learned a lot lending an editorial hand here:

MIT Sloan Management Review, March 3, 2023

by Bernadine J. Dykes, Kalin D. Kolev, Walter J. Ferrier, and Margaret Hughes-Morgan

Given the panoply of recent disruptions — including COVID-19, inflation, Russia’s invasion of Ukraine — it’s no surprise that many leaders are striving to quickly dial up the agility level of their companies. Indeed, the ability to rapidly adapt to changing conditions can be a shield against disruption and a healing prescription for crisis. But organizational agility is not a panacea. There are pitfalls in the pursuit of agility that can and do produce unintended consequences.

Agility is a multidimensional concept that comprises three sequential and interrelated processes: alertness to the need for change, the decision to make the change, and the mobilization of the organizational resources required to execute the change. Our agility research and observations regarding the behavior of companies, especially during the pandemic, revealed that each process contains a pitfall that can subvert its outcomes: Alertness harbors the pitfall of hubris, decision-making harbors the pitfall of impulsiveness, and mobilization harbors the pitfall of resource fatigue. Read the rest here.

Wednesday, January 25, 2023

Rethinking Hierarchy

Learned a lot lending an editorial hand here:

MIT Sloan Management Review, January 25, 2023

by Nicolai J. Foss and Peter G. Klein

Chris Gash/theispot.com

For all the hype and promise swirling around the idea of eliminating management to create agile, flat organizations, bosses and corporate hierarchies have remained extremely resilient. As we argued in the pages of MIT Sloan Management Review in 2014, under the right conditions, having such hierarchies in place is the best way to handle the coordination and cooperation problems that beset human interactions. They allow human intelligence and creativity to flourish on a larger scale. They provide a larger structure, with predictability and accountability, for specialists to do their work.

But that doesn’t mean traditional, command-and-control organizations are right for today’s environment. We see a confluence of business and social trends influencing the development of new kinds of hierarchies. Rapid technological progress, instant communication, value creation based on knowledge rather than physical resources, globalization, and a more educated workforce require us to rethink how we wield managerial authority. Meanwhile, individual views on politics, religion, and culture also inform our attitudes toward hierarchies — such as whether we value autonomy or admire authoritarian figures. All of these factors point to a new, different role for hierarchy to play in meeting the challenges of the 21st century.

The key challenge for designing and operating hierarchies today and tomorrow is to balance two opposing forces. The first is the desire, common to us all, for empowerment and autonomy, which helps companies mobilize employees’ creativity and exploit their unique knowledge and capabilities. The other is the need — particularly in environments characterized by rapid change and interdependent activities across the enterprise — to exercise managerial authority on a large scale.

Companies need clear, fairly enforced policies and procedures that achieve coordination and cooperation while respecting employee desires for empowerment and relative autonomy. Managers have to figure out when to intervene and when to let employees handle problems themselves.

These are tough issues without easy solutions. Which decisions should be decentralized (or delegated)? How much discretion should employees have over the decision areas delegated to them? How are these employees incentivized and evaluated? How do executives make sure that all these decentralized decisions mesh together? A central lesson of theories and evidence on organizational structure is that there are no universally “best” answers to these questions, only trade-offs that depend on the contingencies facing the company. Identifying and acting on those trade-offs — not decentralizing everything, everywhere — is the key to successful leadership. Read the rest here.

Tuesday, January 10, 2023

Can bossless management work?

strategy+business, January 10, 2023

by Theodore Kinni

Photograph by Tom Werner

If you’ve been feeling like your leadership contributions are underappreciated, add a copy of Why Managers Matter to your reading list. In it, Nicolai Foss, a strategy professor at the Copenhagen Business School, and Peter Klein, the W.W. Caruth Chair and professor of entrepreneurship at the Hankamer School of Business, Baylor University, examine the various iterations of manager-free organizations that have been proposed—and occasionally adopted—over the past 50 years or so. Their conclusion: nonsense!

Foss and Klein lump the ideas of management thinkers, such as Gary Hamel, Michele Zanini, and Frederic Laloux, and approaches to decentralized management, such as holacracy and agile, into what they call the bossless company narrative. “The basic thrust of the genre is that while bosses are still around, the less control they exercise the better,” they write. “What the Harvard historian Alfred D. Chandler Jr. called the ‘visible hand’ of management should give way to worker autonomy, self-organizing teams, outsourcing, and an egalitarian office culture.”

Then the duo bales the entire genre into something resembling a straw man and puts a match to it. “The near-bossless companies—and there aren’t many of them—with their self-managing teams, empowered knowledge workers, and ultra-flat organizations are not generally or demonstrably better than traditionally organized ones,” declare Foss and Klein. “Bosses matter, not just as figureheads but as designers, organizers, encouragers, and enforcers.”

Foss and Klein make a detailed and extended case against the bossless company narrative with which it is hard to take issue, especially in the realm of large enterprises. Schemes like holacracy, in which decisions are made by teams, may work for small companies with distributed ownership, such as boutique consultancies and other kinds of partnerships, but they haven’t worked in large companies like Zappos, which have many more employees and require far more coordination. Agility, too, tends to work better for running projects than for running whole companies. In short, hierarchical management structures are, as the authors put it, “the worst form of organization—except for all the others.” Read the rest here.

Tuesday, January 3, 2023

Bad Apples or Bad Leaders?

Learned a lot lending an editorial hand here:

MIT Sloan Management Review, January 3, 2023

by Charn P. McAllister, Jeremy D. Mackey, B. Parker Ellen III, and Katherine C. Alexander

Leaders typically take responsibility when employees perform poorly but not when employees behave badly. It’s like there’s an unwritten rule that protects leaders when employees engage in deviant workplace behavior. Perhaps this protection stems from the notion that it isn’t fair to hold leaders accountable for the actions of a few bad apples.

Our research suggests that surprisingly often, this view of workplace deviance is misguided. We’ve found that leaders have a strong effect on whether employees engage in deviant behaviors. Thus, when employees act badly, their leaders would be wise to take a step back and consider whether and how they may be complicit in that behavior.

Workplace deviance includes employee behaviors that violate organizational norms in ways that threaten the well-being of companies and their employees. Sometimes these behaviors are directed toward individuals, such as when an employee physically or verbally lashes out at a colleague or gossips with coworkers. Other times, deviant behaviors are directed toward an organization, such as when an employee steals workplace property or leaks confidential company information. The consequences of workplace deviance include productivity and inventory losses, as well as a host of other expenses that ultimately cost organizations billions of dollars annually.

Some leaders dismiss workplace deviance as an unavoidable side effect of apathetic or rebellious employees who either don’t care for or actively dislike their colleagues or employers. These bad apples do exist. Research shows that employees low in the personality traits of conscientiousness and agreeableness are more prone to workplace deviance. So are employees who exhibit socially malevolent personality markers referred to as the dark triad: Machiavellianism, narcissism, and psychopathy.

Given these findings, it’s easy to conclude that the “bad apple” argument makes sense. The problem is, research into the role of personality in workplace deviance does not consider the role that leaders play in employee behavior. Read the rest here.

Monday, December 19, 2022

The Transparency Problem in Corporate Philanthropy

Learned a lot lending an editorial hand here:

MIT Sloan Management Review, December 19, 2022

Despite increasing demands by employees, investors, and communities for environmental, social, and governance transparency, philanthropy remains an often overlooked and almost entirely opaque sphere of corporate activity. This is no small issue: In 2021, corporate giving in the U.S. alone is estimated to have exceeded $21 billion.

To explore the dimensions of this problem and understand the use of disclosures in corporate philanthropy more broadly, I studied transparency in the philanthropic foundations of Fortune 100 companies. These foundations are only the tip of the iceberg in corporate giving, but they are indicative of the state of philanthropic transparency across the business world. The research revealed the difficulties that leaders and stakeholders face in trying to gauge the efficacy of giving, ensure accountability for it, and capture the full value it may offer to both the givers and recipients of corporate largesse.

Sixty-seven Fortune 100 companies operate active private foundations. In 2019, their combined grants approached $2.3 billion, which was directed to a variety of causes, including health and social services, community and economic development, education, civic and public affairs, arts and culture, the environment, and disaster relief.

There is no comprehensive set of disclosure protocols for company-sponsored foundations in any of the major international standards, such as the Global Reporting Initiative’s sustainability reporting framework. However, there is an extensive set of disclosure protocols for foundations in the nonprofit sector, including having a searchable grants database, sharing a categorized grant list, and providing online access to the 990-PF tax forms they file, which list grant amounts and the names of their recipients.

My analysis of the foundation and corporate websites of the Fortune 100, as well as their foundation and corporate social responsibility (CSR) reports, revealed that the vast majority of the companies do not follow any of the three protocols (a searchable database, a categorized grant list, or online 990-PFs). Only 4.5% of the companies provide a searchable grant database, only 7.5% offer a categorized grants list, and just 7.5% provide online access to their 990-PF filings. Read the rest here.

Tuesday, December 13, 2022

Employee resource groups are more than “food, fun, and flags”

strategy+business, December 13, 2022

by Theodore Kinni

Photograph by MoMo Productions

In 1964, in the aftermath of race riots in Rochester, New York, Joseph Wilson, the CEO who transformed the Haloid Photographic Company into Xerox, invited Black employees to come together to address and remedy racial discrimination within the company. This group evolved into the National Black Employees Caucus, the first employee resource group (ERG). A half-century later, ERGs are a ubiquitous feature of the corporate landscape.

“ERGs have formed within the workplace to support and represent people with identities and demographics related to gender, race, sexual orientation, ability/disability, caregiver roles, military status, religious affiliation, generation, geographic area, job function, and more,” writes diversity, equity, and inclusion consultant and coach Farzana Nayani in The Power of Employee Resource Groups. In this handbook, Nayani offers practical advice to leaders of companies and ERGs who want to ensure that the time and resources they invest in their own groups are well spent.

“There is much debate as to whether affinity groups and ERGs are simply there to celebrate ‘food, fun, and flags,’” writes Nayani. But that’s a reductionist view, she says, one that ignores a host of potential benefits ERGs can provide to employees, companies, and communities. Nayani ticks them off: support, opportunities, and a voice for marginalized employees; enhanced leadership development and innovation pipelines; better employee engagement; increased reputational capital for the company; and more inclusive and socially responsible corporate behaviors that can deliver dividends to the communities in which businesses operate.

The key to achieving these benefits, says Nayani, is forging an explicit connection between a company’s ERGs and its organizational goals in five areas: workforce, workplace, marketplace, community, and suppliers. “Each of these five pillars is an area of focus where employee resource groups can offer contributions and also receive the benefits of efforts focused on the key themes,” she adds. Read the rest here.

Tuesday, December 6, 2022

Preparing Your Company for the Next Recession

Learned a lot lending an editorial hand here:

MIT Sloan Management Review, December 6, 2022

by Donald Sull and Charles Sull

Winter is coming: Inverted yield curves, rising interest rates, and a rash of layoff announcements have convinced many economists that the global economy is headed for a downturn. Recessions are bad for business, but downturns are not destiny.

The worst of times for the economy as a whole can be the best of times for individual companies to improve their fortunes. One study found that lagging companies are twice as likely to overtake industry leaders during a recession, relative to nonrecessionary periods. Another study, of nearly 4,000 global companies before, during, and after the Great Recession, found that the top decile of companies grew earnings by 17% per year during the downturn, while the laggards saw profits stagnate or decline. The difference between the companies in the two groups translated into $6 billion in enterprise value on average.

How can the same recession cause some corporate empires to rise and others to fall? The short answer is that uncertainty surges dramatically during recessions — increasing roughly threefold at the company level compared with the relative calm before or after a downturn.

“Chaos isn’t a pit,” explains Petyr “Littlefinger” Baelish in Game of Thrones. “Chaos is a ladder.” The chaos of a recession, however, is both a pit and a ladder. In the face of uncertainty, some companies retrench. They abandon attractive customers and promising markets, offload valuable assets at fire sales, cut prices, and seek new partners to bolster cash flow. Others start climbing. They seize opportunities and improve their fortunes.

Our research has identified three fundamental ways to manage uncertainty: resilience, local agility, and portfolio agility. Leaders can take a series of steps, such as building a strong balance sheet or diversifying cash flows, to boost an organization’s resilience and ability to withstand environmental shocks. Local agility is the ability of individual business units, functions, product teams, and geographies to respond quickly and effectively to changes in their specific circumstances.

Portfolio agility is an organization’s capability to quickly and effectively shift resources across different parts of the business. While local agility enables individual teams to spot and seize opportunities, portfolio agility enables the company as a whole to double down on its most promising investments. Portfolio agility is, by some estimates, the largest single driver of revenue growth and total shareholder returns for large companies. Quickly and effectively reallocating resources is valuable at any point in the business cycle, but it’s decisive during downturns, when internal cash flows dwindle and access to external funding dries up.

Resilience and agility are effective in isolation, but in combination, their impact is turbocharged. In the midst of a downturn, resilient companies can weather the storm to wait for opportunities to arise. Having a high level of resilience — by building a war chest of cash or obtaining secure access to funding — provides an organization with the wherewithal to fund emerging opportunities, but only if it is agile enough to seize those opportunities. Resilience without agility may ensure survival but will not position a company for future growth. Agile companies without resilience, in contrast, often lack the resources to exploit the opportunities they spot. Read the rest here.

Monday, November 7, 2022

Get Ready for the Next Supply Disruption

Learned a lot lending an editorial hand here:

MIT Sloan Management Review, November 7, 2022

by M. Johnny Rungtusanatham and David A. Johnston

Michael Austin/theispot.com

The COVID-19 pandemic has ushered in an era of supply chain disruption and unpredictability that has severely challenged many companies’ planning and processes, and revealed how far prevailing practices are from the ideal. An MIT Center for Transportation and Logistics poll conducted online at the onset of the pandemic revealed that only 16% of organizations had an emergency response center — an established best practice for mitigating and recovering from unplanned interruptions in the physical flow of goods.

Unsurprisingly, given the pandemic’s disruptive effects, the same poll found that the highest ambition of supply chain managers was to bolster their risk management protocols and tools. The problem with crisis-driven supply chain initiatives that are focused on protocols and tools is that they are only as effective as the ability of the organization to use them. Having that ability requires the systematic development of capabilities to manage for supply disruptions. These capabilities are combinations of people, policies, processes, and technologies that ensure companies can not only plan for and respond to known business and operating risks but also — and more importantly — manage unknown-but-knowable threats and their associated consequences.

We’ve identified six capabilities that fill this bill: anticipate, diagnose, detect, activate resources for, protect against, and track threats. Together, they constitute the ADDAPT framework, which is based on our research into how public agencies and private enterprises experience and respond to supply disruptions like the COVID-19 pandemic. In medicine, pathology is aimed at understanding the causes and effects of a disease to guide treatment. Similarly, the ADDAPT capabilities help companies understand the causes of supply disruptions and their immediate and long-term effects, in order to both respond to unfolding supply disruptions and prevent their recurrence. Read the rest here.

Tuesday, October 18, 2022

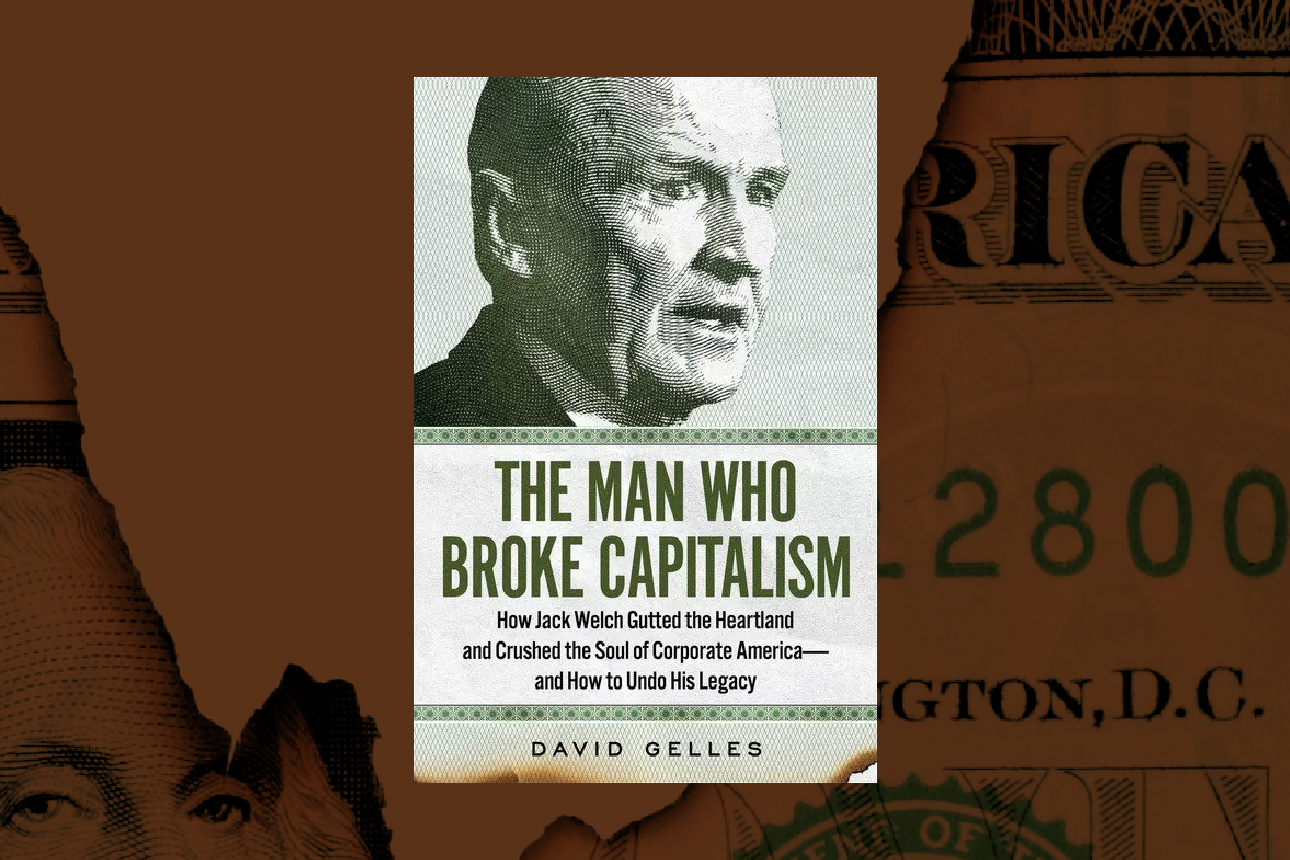

Did Jack Welch Blow Up the Business World?

MIT Sloan Management Review, October 18, 2022

by Theodore Kinni

“The history of the world is but the biography of great men,” wrote 19th-century Scottish historian Thomas Carlyle. With The Man Who Broke Capitalism, New York Times business reporter David Gelles attempts to resuscitate the hoary “great man” theory of leadership in a backhanded sort of way. He calls out the late Jack Welch, the General Electric CEO whom Fortune magazine anointed “manager of the century” in 1999, as the evil mastermind behind the litany of economic woes rooted in shareholder capitalism gone wild, but he pays scant attention to their root causes.

When Welch took up the reins at GE in 1981, it was not a prosperous time in America’s economic history. The post-World War II boom was on its last legs: America’s industrial giants were sinking under their own weight, and foreign companies, especially those from Japan and Germany, were making inroads the size of superhighways into the U.S. consumer market. GE, then one of the nation’s leading companies, was languishing in the slow growth environment too.

If you were in business in the 1980s and ’90s, Gelles’s recounting of Welch’s tenure at GE will be a familiar story. “Neutron Jack” cut head count and instituted an annual employee ranking scheme that required that employees in the lowest decile be fired. The company’s business units had to be No. 1 or 2 in their market or they were jettisoned. Meanwhile, Welch chased new growth opportunities in financial services and media — soon, GE Capital alone accounted for more than half of the company’s profits.

The results? “During [Welch’s] tenure, GE posted annualized share price growth of about 21% a year, far outpacing the S&P 500 even during a historic bull market,” writes Gelles. “When Welch took over, GE was worth $14 billion. Two decades later, the company was worth $600 billion — the most valuable company in the world.” Read the rest here.

Tuesday, September 13, 2022

Manage Your Customer Portfolio for Maximum Lifetime Value

Learned a lot lending an editorial hand here:

MIT Sloan Management Review, September 13, 2022

by Fred Selnes and Michael D. Johnson

Traci Daberko/theispot.com

When we wrote about customer portfolio management (CPM) and our research into customer portfolio lifetime value (CPLV) for this publication in 2005, we emphasized the need to balance a “large, leaky bucket” of weaker customer relationships alongside closer and higher-value customer relationships. But according to our latest research, there is much more that businesses can and should be doing to drive future revenue. These actions depend on both market conditions and a company’s resources.

Growing a company’s customer portfolio requires continual investments across a range of weaker to stronger relationships. Our updated CPLV model shows that a clear understanding of when and how much to invest in, leverage, and defend different customer relationships is an essential determinant of both current and future revenues and costs.

Most companies lack a basis for developing this understanding. Business leaders seeking to optimally manage the ecosystem of customer relationships face a complex problem — and for most, de facto CPM practices are more likely to focus myopically on either current sales or their most valuable customers. However, our model shows that what’s really required is to integrate multiple dimensions (not just scale, but also variances in customers’ needs and wants) and tactics (relationship conversion, leverage, and defense) across the whole customer portfolio.

Our CPM framework and CPLV model enable executives to answer the following key questions as they seek to grow and optimize their company’s customer portfolio:

- How central is developing customer relationship strength to our strategy and competitive advantage? More specifically, when and how much should we invest in converting weaker relationships to stronger relationships?

- How do we leverage these investments once relationships are created?

- How do we protect the relationships we have created to minimize customer churn?

Our CPLV model illuminates how these relationships relate to the value proposition of a company by predicting a seller’s future revenues from and costs associated with the different relationship segments. These predictions are based on a set of parameters that includes market growth over the course of a product life cycle, unit cost over time, the cost and probability of deepening relationships, relationship premiums, and switching costs and probabilities. By running extensive simulations within the model, we have identified three explicit goals for an effective CPM growth strategy: relationship conversion, relationship leverage, and relationship defense. Read the rest here